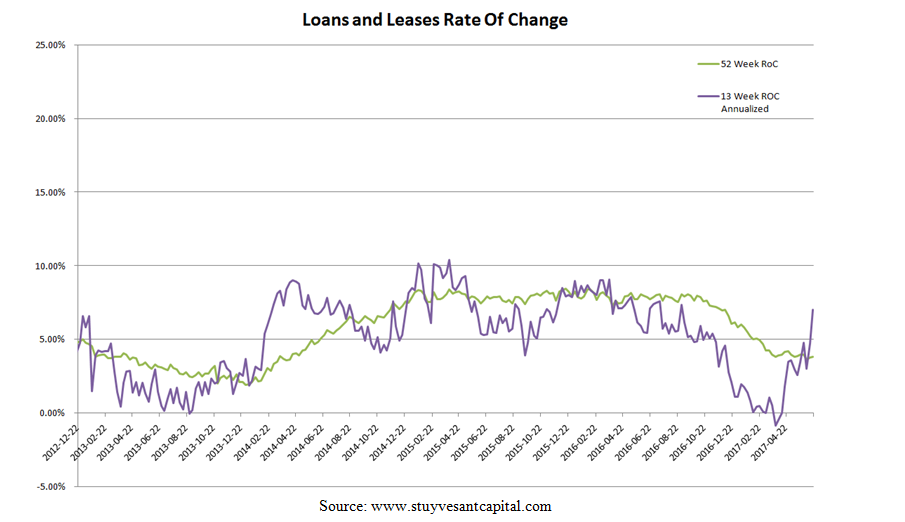

Stuyvesant Insight: Reflation Before Inflation

/Reflation implies an increase in the rate of inflation from below trend towards the Fed's long-run inflation goal of 2.0%. It is often fueled by fiscal and / or monetary stimulus, which serves to increase aggregate demand. The reflation trade that began in late 2016 was catalyzed by market hopes that deregulation, tax cuts, and infrastructure spending would be quickly implemented after the 2016 Presidential election. This resulted in cyclicals / value stocks significantly outperforming their defensive / growth counterparts. This trade reversed due to disappointing first quarter GDP (1.2%) and the now uncertain implementation of Trump's platform. In spite of this a new reflation trade was born.

The new reflation trade is a result of the decline in the price of WTI crude oil, the US dollar, and long-dated Treasury yields in the first half 2017. This is a powerful combination for increasing for final demand. Effectively, this serves as a tax cut to workers via an increase to real disposable income (decreasing the percentage of household income directed to the non-discretionary oil-related outlays); an increase in global demand for our goods and services via devaluation of the dollar; and a decrease in the cost of capital investment due to the decrease in borrowing costs, which should support fixed capital investment. In fact, US economic conditions have become increasingly reflationary despite the Fed tightening monetary policy by increasing the Fed Fund's rate three times over the past eight months (December, March, and June) to a range of 100-125 bps.

This is corroborated by Stuyvesant's Reflation Study, a leading indicator:

The Stuyvesant Reflation Study is calculated as the inverse of an equal-weighted index of Z-scores that are computed for oil prices, 10-year Treasury yields, and the US dollar on a monthly basis. When this index trends above the zero-bound, it indicates that the economy is undergoing a reflationary impulse and when it is below the zero-bound it indicates that conditions are becoming restrictive. A powerful up thrust began in late 2016 and continues through June of 2017. Our study has historically been a leading indicator for the US Economic Surpirse Index shown below:

Citi's U.S. Economic Surprise Index measures the difference between expected economic versus actual data, smoothed over the past three months, weighted for the most recent releases. When data beats analyst expectations the index trends up and when data misses the index trends down. Given the propensity of our reflation study to lead the economic surprise index, we expect that the strong reflationary impulse will lead to positive economic surprises.

The New York Nowcast currently forecasts 2Q17 GDP growth at 1.90% and the Federal Reserve Bank of Atlanta's GDPNow model forecasts 2Q17 GDP growth at 2.5%. We expect US GDP to grow at approximately 2.2% for the second quarter. This is a long ways away from President Trump's 3.0% goal, but is greater than the Fed's projection of 1.8% potential growth. The reflation trade should cause domestic growth to accelerate into the back half of this year. With second quarter economic growth already running above potential and tightness in the labor market (U-6 at 8.6%, which is near the low prior to the Great Financial Crisis), we continue to anticipate that yields will rise in the back half of 2017, led by inflation. Any additional fiscal stimulus, financed through deficit spending, should be construed as a positive surprise and will exacerbate the reflationary trend.